The need to extend the WTO TRIPS pharmaceuticals transition period for least developed countries in the Covid-19 era: Evidence from Bangladesh

New UN policy brief (pdf) with Prof. Kevin Gallagher of Boston University.

Abstract

Bangladesh is one of the most successful least developed countries (LDCs). The country has made such strides that in 2021 the United Nations Committee for Development Policy will consider whether it should graduate out of the LDC category altogether. Like few others, Bangladesh took advantage of WTO flexibilities to build a vibrant pharmaceuticals industry that provides needed industrialization and employment. The pharmaceuticals industry also gives access to essential medicines to millions of Bangladeshis as well as people in other developing countries and LDCs. LDC graduation would bring a loss of WTO exceptions, particularly in intellectual property. This policy brief synthesizes recent research, showing that Bangladesh’s vital pharmaceutical industry would be threatened if the country had to adhere fully to WTO rules upon LDC graduation. Given that COVID-19 has dealt such a severe blow to Bangladesh’s development and health prospects, these papers point to the need for Bangladesh to be able to maintain its WTO flexibilities in order for the sector to remain a source of economic growth and health provision in the years to come.

Building the world back realistically

My last post on the need to build the world back better said that most discussion of the post-covid recovery is mistakenly confined to national borders and should have a global dimension.

It’s a view that could be read as idealistic and naive. The world is retreating from physical globalisation. Building the world back better is probably far from most people’s minds.

The G20 can’t even coordinate itself as it did during the last crisis. The world’s multilateral institutions are under attack: the World Trade Organisation and the World Health Organisation, and more broadly the United Nations. Europeans squabble. The United States and China are Punch and Judy.

But even if world leaders look like they’re intent on turning back the clock rather than building back better, it’s at least worth saying something. As I said in the conclusion to my post, sometimes things change quickly.

For progressives or internationalists it’s also important to think about how and why change happens. The cynic who imagines everything always gets worse is just as inaccurate as the relentless optimist. We’re not heading for an entirely splintered, uncoordinated world where all countries shut in on themselves.

Progress occurs, but it has to be fought for. Who’d have thought a couple of months ago that US protests against police discrimination and violence could have shut down a police department and spread worldwide? Certainly not me.

The end of segregation and votes for black people and women – as ordinary as these outcomes can now sound – were hard-fought struggles against entrenched reaction and commercial interest which echoed around the world. The anti-apartheid movement wasn’t assured of success.

At one time the idea of most countries signing a charter urging world peace and harmony would have sounded silly – yet that is what the United Nations is (with all its shortcomings): a popular attempt at a punctuation mark on mass, mechanised death – supported, of course, by powerful lobbies and nations whose interests it served.

The Treaty of Rome in 1957 had democratic and elite support. It led to the longest period of peace in modern European history.

So positive international change happens and it can be grand in scale, even if progress is far from guaranteed and has to be fought for in order for it to benefit ordinary people rather than only the powerful. The interests of the 1% can at times be made to coalesce with those of the rest of us.

It’d be wrong to imagine that recent trends toward nationalism or insularity can only lead one way, even if further fragmentation looks likely and things can deteriorate across time or place.

At times of stress things can pivot one way or another, making it more important than ever to put ambitious ideas on to the agenda and for good people who’d otherwise do nothing to get off their backsides.

Useful change is usually the result of thoughtful people engaging in protest and democracy, with coherent political objectives: pressure from below, with an eye beyond national borders.

Back on the idealistic subject of the need to build the world back better, it’s important not to see things in binary. Globalisation will moderate and perhaps retreat, but it won’t end. It benefits large, rising powers like China, which needs the high-spending United States to buy its exports. Americans need somewhere to make their stuff, cheaply. And integration was obviously to the advantage of the United States and European corporations in recent decades.

Goods trade will probably continue to stagnate or wobble. Supply chains are shortening after Covid-19. Environmental concerns are prompting some to ask why goods need to be shipped so far.

Robots will take over some jobs from workers, so there’s less need to make products on the other side of the world. America and Europe won’t need to make so many goods in China (even if they still make a lot of things there).

But multinational companies need lower barriers to trade and investment. States usually adapt to the demands of capital.

The institutions that facilitated and accompanied the last phase of globalisation won’t just crumble. They’re needed to smooth the flow of capital and trade with rules and norms for commerce.

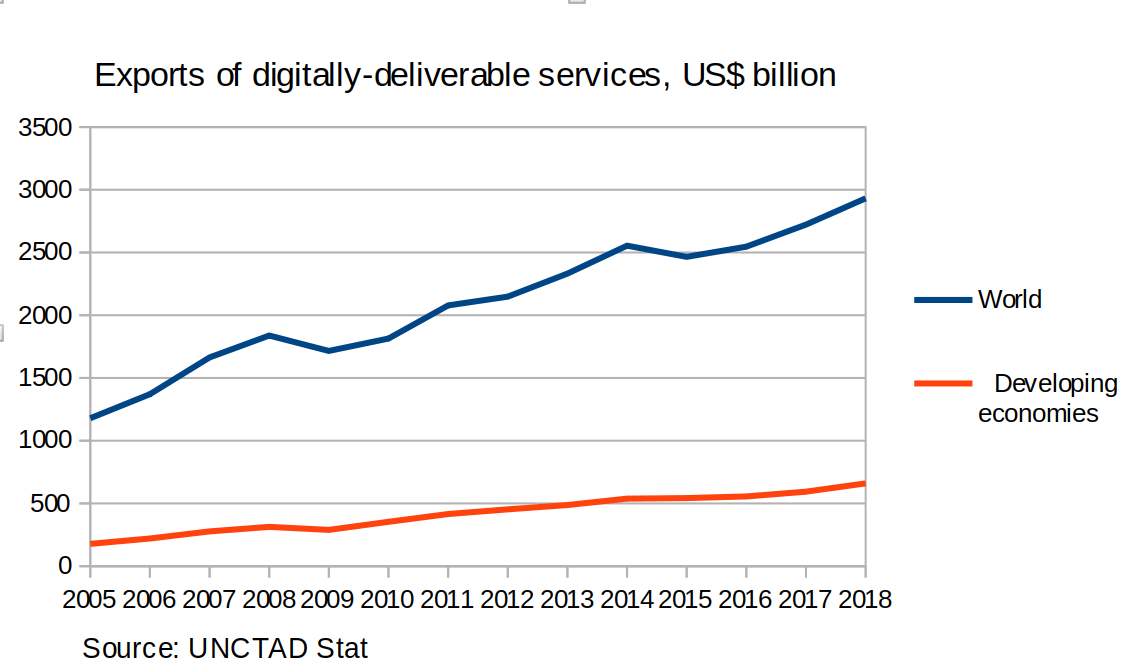

A small but significant chance exists that new global institutions emerge to service the changed environment, just as during previous crises. New types of global governance might centre around the digital economy where so much trade now takes place.

International digital trade is largely unregulated but some argue we’re at the start of a new era — like the age of steam, container ship or airline.

Companies (mostly big ones in the US, Europe and increasingly China) will demand protection of their intellectual property. They’ll need rules for selling their stuff to other countries, which needs legislation and common formats. The current talks on digital trade at the World Trade Organisation are among the most interesting and important.

A shift to a new, online, less labour-intensive type of globalisation might already be happening – although any shift won’t be absolute, and shoppers in the rich world will for a long time still want to take advantage of cheap labour in poor countries.

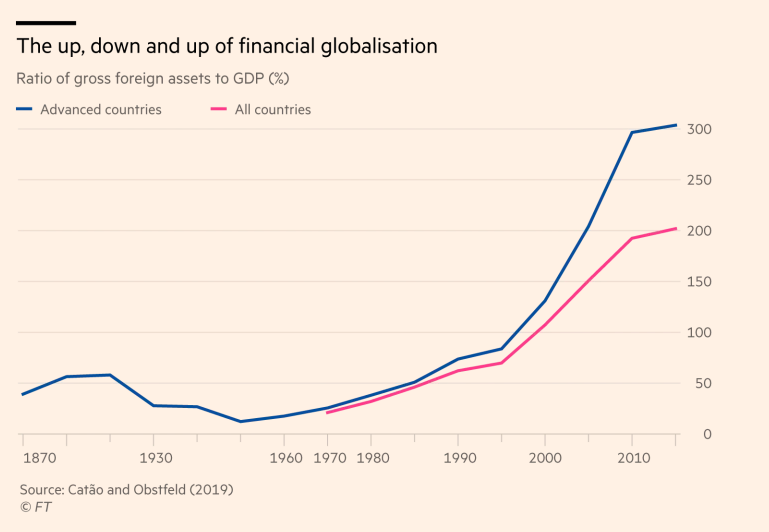

Unfortunately financial globalisation is rushing ahead. That sort of integration has boomed in recent years and doesn’t necessarily look like slowing down nor being regulated better. The world economy will remain a casino for financial market speculators.

Source: Financial Times, H/T @DanielaGabor

What’s likely is that we’re seeing the ending of one phase of international consolidation and the dawn of another. It needs to be bent toward the needs of the majority.

Build the world back better

Bike lanes are all very well, but it’s global change that really counts.

At a time when politicians and commentators are talking about the need to rebuild more sensibly after Covid-19, it’s more important than ever to think globally. Most recent health, economic and environmental crises were international, and so must be the remedies. This view isn’t misty-eyed one-worldism; it’s self-preservation.

Pandemics like Covid-19 are inherently global. The first death was reported on January 11. Ten days later the virus was being treated in half a dozen countries. The pathogen’s spread has now made it more lethal than any other in nearly a century.

The only way to tackle it successfully is to coordinate the international response, sharing information on its causes and proliferation, and collaborating on containment and vaccines.

Heading off any future potential viral outbreaks at source would be the best way of preventing more crises. The next Covid will probably come from the developing world. This means large-scale coordinated international humanitarian and development assistance in zones of potential concern — before the fact, not after.

Ebola, for instance, was a story of poverty and over-stretched West African health systems as much as it was a terrible new illness. Communities and hospitals simply couldn’t cope. The prospect of such a disease reaching the scale of Covid is even more horrifying than the original catastrophe.

Investment in vulnerable countries’ economies, national revenue collection and health systems needs to be scaled up — not only an act of caring, but a form of insurance against future disasters.

A further reason to think and act globally is that health and environmental shocks are connected. Ebola and Covid can be traced to the invasion of isolated ecosystems and to over-intensive farming techniques.

Humans are exploiting animals to unprecedented levels and intruding more and more on the habitats of previously less-contacted species. Without joined-up thinking, separate health and environmental initiatives will simply fall short of objectives.

Three out of four new infectious diseases come from animals. Covid has been linked to bats and Pangolins in East Asian meat markets.

According to the UN Environment Programme: “[The] Ebola outbreak in West Africa was the result of forest losses leading to closer contacts between wildlife and human settlements; the emergence of avian influenza was linked to intensive poultry farming; and the Nipah virus was linked to the intensification of pig farming and fruit production in Malaysia”.

It’s long been clear that global and local pressures on the environment must be addressed internationally. Just as burning and logging the Brazilian rainforest amounts to destruction of the world’s biggest carbon sink, so too, Chinese, European and US emissions in effect cause coastlines on the other side of the world to be swamped.

The largest carbon emitters can each make a difference on their own, but no single country will do so without another first committing, which is why a commonly-negotiated binding agreement is so essential.

And it’s no good folk in the rich world thinking they’ll stop domestic flooding only by recycling more or installing bike lanes. Enlightened though such moves are, global carbon cuts will have an incalculably larger benefit.

In the same way that climate breakdown blows back on the rich in the form of health and national environmental emergencies, so does global poverty itself. The main reason Europe has recently faced such large refugee inflows is that some people from poor or unstable countries understandably want to leave.

Immigrants are in reality good for the countries they arrive in, working hard in the jobs locals don’t want to do and forming a valuable source of dynamism and entrepreneurship.

But no-one wants to fester in a refugee camp. And anti-immigration sentiment is easily manipulated by short-sighted populists; arguably the biggest current scourge of the rich world.

As mercenary as it sounds, reducing poverty at source and reducing overseas conflict would make it safer and more attractive for poor people to stay at home and help them live more sustainably.

Poor communities are often the guardians of the natural environment on which the rich countries depend. The Kayapo and other Brazilian tribespeople defending their areas of the rainforest from logging and mining are in effect acting on behalf of the world. Pacific islanders who protect their seas from illegal fishing safeguard two-thirds of the earth’s surface.

Conversely poverty can lead to unsustainable exploitation of the natural environment. Deforestation and illegal mining, for example, are partly economic in origin, as people search for fuel and income. Drought and flooding also contribute to emigration.

Economic instability makes for an increasingly global undertow to health and environmental stress. Economic crises have been deepening and becoming more regular, and globalisation has synchronised the cycles of several markets, regions and countries which used to be relatively independent.

A currency wobble soon becomes a financial meltdown, and before long a worldwide economic downturn. As we’re now finding out, environmental, refugee and health problems become more acute amid growing poverty and insecurity.

Depending on how you define the term, a crisis has struck about once a year since 1990, beginning with widespread recession among developed countries, a series of national calamities, then the Asian collapse and the Russian devaluation and default toward the end of the decade.

The 2000s kicked off with the recession brought on by the bursting of the dotcom bubble – then turmoil really got going with the 2007-2009 global economic crisis and the fallout across Europe. This rocky road ended in 2020 with the worst economic crash in centuries, the impact of which will play out for many years.

New foundations

These health, environmental and economic convulsions are inherently linked. They can’t be addressed by one nation alone behind closed borders. As unlikely as it currently sounds in a fragmenting world, the only answer is common action using fit-for-purpose global rules and institutions.

A global green new deal is critical, reflating the world economy with sustainable infrastructure ready to serve people and the planet. Not only must the Paris climate targets be met, but policies put in place to reduce carbon dependency, protect ecosystems and water resources, and alleviate poverty.

UN reform is a prerequisite for such an ambitious programme, starting with full representation of all of the world’s regions on the Security Council rather than only the five powerful nations that won the second world war.

Other than China, no Asian country is a permanent member — nor any African or Latin American nation. Concerted and unified pressure from these rising regions can lead to real change.

The UN Sustainable Development Goals, worthy though they are, are now beginning to look over-ambitious, with not enough done to ensure compliance. The machinery for implementation needs to be put in place before it’s too late.

One of the most sensible ways in which the rich world could build back better would be to get its own economic house in order, ending the financial lawlessness that leads to worsening crises. This means resetting the monetary system, with coordination of global macroeconomic policy, exchange rate management and capital flows.

As part of this reset, leadership of the World Bank and International Monetary Fund – at the helm of the global economy – needs to change so that all countries are properly represented in leadership, ending the anachronism whereby Europe and the US split leadership between them.

Radical options to be re-explored include an international clearing union, world currency and global minimum wage.

Further taxing international financial transactions would throw sand in the wheels of international flows and deter speculators. This is particularly needed in the case for commodity derivatives speculation, which directly causes poverty and hardship.

Instead of the world having to bail poorer governments out so often and write off loans, it would be better to avoid the conditions that created the debt in the first place, which include forcing austerity policies on to poor or emerging countries, making them reliant on international capital markets and making it difficult for them to earn foreign exchange. The UN has even proposed a sovereign debt forum and an international mechanism for restructuring sovereign debt.

Broad-based support for the least developed countries would help head off future health and environmental ructions at source and cushion the impact on the worst off. This support needs to encompass trade, investment, commodities, technology and climate breakdown.

Some have even proposed a Marshall Plan for health, with wealthy countries clubbing together to kickstart mass investment in health infrastructure among poorer nations.

If all of this sounds ambitious, that’s because it is. The very foundations of the world are creaking, and this parlous state demands unified health, environmental and economic action. Weakness and indecision will only lead to further division, heralding yet worse calamity.

Crisis need not feed on itself. Enlightenment can spring from the darkest places. Just as the old international system emerged from the second world war, extreme stress can, against the odds, bring new beginnings.

As Lenin said, there are decades where nothing happens and weeks where decades happen. Instead of waiting for the weeks when a crumbling house turns to dust, it would be better to start rebuilding now.

To get LDC graduation back on track, and to help other LDCs, reform of the international system of support must be fundamental and far-reaching.

At the start of 2020, a dozen least developed countries (LDCs) were on schedule to leave the category by the middle of the decade. That timetable now looks uncertain.

COVID-19 has exacted an unprecedented human toll as underprepared health systems struggle to cope and workers in lockdown lose their livelihoods. Many economies are collapsing as demand for exports falls, tourism tumbles and remittances slump with the repatriation of foreign workers. As LDCs and others struggle to balance their books, global financial turbulence looms.

The UN Committee for Development Policy (CDP), the body responsible for monitoring the category and recommending countries for graduation, is consulting governments about what action to take. No decision has yet been made to delay any country’s graduation or to put in place longer transition periods. But a range of outcomes are possible.

Source: Committee for Development Policy Secretariat

*ECOSOC: UN Economic and Social Council

Six countries were close to meeting the UN criteria for graduation for the first time: Cambodia, Djibouti, Lesotho, Senegal, Togo and Zambia. Coronavirus will slow their progress.

The current downturn shouldn’t be seen as a one-off, with LDCs bouncing back quickly. The 2007-08 global economic crisis suggests that LDCs will take years to recover.

Global health, economic and environmental crises are becoming more frequent, and the fallout for LDCs regular and calamitous. Even before the current shock, LDCs suffered worse than most from trade, financial and commodity price volatility, cyclones, droughts and other disasters.

Not enough has been done to make LDCs more resilient or to boost incomes. In a paper published by the Commonwealth Secretariat last month, I argue that the support measures for LDCs could be much more ambitious.

A comprehensive overhaul of the system of international support needs to aim not only at the 18 countries at or near the graduation threshold, but the other 29, many of which in recent years have become more vulnerable and moved even further from graduation.

The recovery from COVID-19 represents a chance to put in place deep-rooted, systemic improvements to the multilateral architecture relating to LDCs – driven by LDC governments themselves and differentiated according to context.

While existing support for LDCs is welcome, any new support architecture should be much more extensive, running across six areas:

1. The international system

UN entities and institutions such as the World Bank and International Monetary Fund should coordinate LDC-related activities better and use the category more in aid, lending and other decisions. A facility to support graduates, as considered by the CDP earlier this year, would help accommodate differences within the category. Direct assistance should be provided for less-advanced members of the group.

2. Finance and investment

Donors should meet official targets and allocate a higher proportion of aid to graduating countries toward building productive capacities. For all LDCs, new forms of financing need to be approached carefully and strategically. Help with growing public revenues is a bigger priority. Debts should be cancelled during crises as big as the current one; not just interest payments suspended.

3. Trade

World Trade Organisation special and differential treatment (SDT) for LDCs, while useful, could be strengthened. Some types of SDT have already run out or will soon do so, and could be extended. Several countries do not provide full duty-free coverage for LDC exports, while relaxed rules of origin have been shown to benefit LDC exporters. Ecommerce is playing a bigger role in LDC trade – and here the interests of LDCs must remain paramount in bilaterals and multilaterals.

4. Commodities and resources

Commodity price volatility has been one of the worst sources of instability for LDCs, and a series of innovative proposals has been made to smooth prices, including a counter-cyclical financing facility; transactions taxes; and revitalised ‘smart’ commodity agreements.

5. Technology

The new technology bank for LDCs was launched on a small budget and should be funded better. Knowledge and dissemination of technology in LDCs needs to be encouraged through the transfer of corporate personnel.

6. Climate breakdown and environment

LDCs are affected more than most. South-South collaboration could be encouraged more; the LDC climate fund replenished; and financing made more accessible. The administrative requirements for funding are often too great for small, capacity-constrained countries. Disaster resilience could be made more pre-emptive and built into infrastructure in advance, rather than addressed only via insurance.

Without far-reaching reform to international support, any hope of meeting graduation targets will be in vain. The COVID-19 downturn will take many years to play out. To get things back on track, the world needs to help cushion the impact of this crisis and shield LDCs from future ones.

———————

Download the paper here.

—————————–

A webinar on 28 May 2020 will be covering LDC graduation and COVID-19’s impacts, hosted by EIF and the Commonwealth Secretariat. Register here.

First published on EIF Trade for Development News.

Until early this year the Pacific islands were a rare ray of sunshine for the international development system. The region’s four least developed countries (LDCs) were among the first of a dozen nations newly scheduled to leave the UN category for the most vulnerable low income states.

Led by Vanuatu, which is scheduled to graduate in December 2020, these countries benefited from years of relative regime stability, tourism growth and solid health and education policies. Solomon Islands is scheduled to graduate in 2024. Kiribati and Tuvalu also meet the criteria.

Covid-19 has thrown a shadow across the region, cutting off the tourism on which most rely. Restrictions on movement have disrupted domestic activity. The collapse in the world economy has slashed demand for exports and forced foreign workers to go home. Global financial calamity threatens, as countries in and outside the region struggle to pay their debts.

In early April yet another tropical cyclone hit agriculture and rural communities in Solomon Islands and Vanuatu.

A poor run of luck? A ‘black swan’ – the term coined by the philosopher Nassim Nicholas Taleb for unknowable high-impact events – compounded by unlucky weather?

In a paper published last month by the Commonwealth Secretariat in London, I argue that vulnerability is an inherent and functional feature of the existing global order. The international community could do much more to support LDCs.

Vulnerability is the norm for these countries. The way the global economy and climate are currently (dis)organised, peripheral countries will always be exposed to shocks.

The Pacific island countries, like others on the global margins, have in the past couple of decades fallen foul of a series of crises that began in the rich world. They included the dotcom crash, an eight year commodity boom that led to huge price increases for imported items such as gasoline and food, a subsequent collapse, resurgence and then even deeper trough in 2016. The global financial crisis in 2008 hit LDCs more than most and small island developing states worst of all, as export demand and tourism slowed.

The rich world’s carbon addiction has played out particularly badly for the Pacific as, on top of sea level rise and the periodic plunder of their natural assets by multinationals, a series of climate cataclysms culminated in cyclone Pam in 2015.

According to the official UN measure of vulnerability, 20 of the 47 LDCs worldwide became more vulnerable between 2015 and 2018.

Covid is only the latest in this nightmarish helter-skelter. The pandemic was no black swan. It was entirely knowable and could have been prepared for: health experts warned for years that health scares were worsening in the wake of bird ‘flu, SARS and MERS.

But global leadership is lacking and the system isn’t set up to prevent crises. One of the best things that the rich world could do for LDCs is get its own house in order, clamping down on the behaviour that leads to worsening global health and economic crises.

But wealthy countries could do much more directly for the least developed. There are three types of help for LDCs: market access, aid, and assistance with taking part in the international system.

The main benefit for LDCs is that in most markets they pay no taxes on exports or restrictions on how much can be sent abroad.

But Pacific island LDCs don’t export many goods. And exports don’t respond magically to falling trade barriers anyway – they depend on domestic productive capacity.

Another support for LDCs is that official donors commit to send them certain amounts of development assistance. While aid per head to Pacific LDCs is among the highest in the world, most donor states fail to meet their pledges.

LDC governments also benefit from a series of other small advantages like free travel to some international meetings and lower payments to the UN budget. All good stuff, but small beer alongside the regular and worsening catastrophes raining down on the region.

In my paper I argue that while this support is welcome, it’s time to think bigger – particularly about economic instability and its impact on the most vulnerable. Systemic change is needed at the multilateral level, with measures to coordinate global markets and better coordination at the UN.

The paper argues for a series of around 30 support mechanisms, covering finance and investment, trade, commodities and resource extraction, technology, climate breakdown and the environment. These measures need to be part of an ecosystem led by LDCs, not offered willy-nilly at the whim of the powerful.

- A measure long argued for, is a tax on international financial transactions to slow the flow of hot money and stabilise the world economy.

- An international financing facility to boost demand in LDCs during crises.

- The evidence shows that direct cash payments to the poor work well, and can provide a buffer for the most vulnerable in society.

- Donors could finance geological information in LDCs so as to avoid multinationals manipulating knowledge about mineral reserves to their own advantage.

- Companies should be made liable for environmental damage incurred in resource extraction, including on the seabed. Such a rule should be enshrined in international law, with independent adjudication determining damages.

- It is imperative to meet climate targets. The climate fund for LDCs is depleted and should be replenished, made less bureaucratic and more accessible.

- Infrastructure should be made disaster-resilient during construction using innovative financing and made part of building productive capacity.

These are just a few of the suggestions in the paper. Business-as-usual just isn’t good enough. Unless the global system of economic governance changes radically and the architecture for LDCs drastically improves, things will continue to get more precarious. The next economic crisis or pandemic could be even worse. And, after a couple of decades of experimentation with globalisation and the market economy, the tried and tested traditional resilience measures of Pacific islanders’ subsistence ancestors will start to look more and more attractive. Pacific leaders might just start questioning their engagement with the wider world.

Originally published in Griffith University’s Pacific Outlook.

New Commonwealth Secretariat International Trade Working Paper:

International support to least developed countries (LDCs) falls in the areas of trade, development cooperation and assistance with participation in the inter-governmental process. With 10 years of the 2030 Agenda to go, and before the fifth 10-year Programme of Action for LDCs starts in 2021, there is a need to re-evaluate the system of international support. Some LDCs are performing well, but key international targets have been missed. On average the contributions of trade and investment remain too low. Several LDC economies are contracting and becoming more vulnerable.

Taking a critical look at the theory and assumptions underlying international support makes it possible to propose new assistance mechanisms, as opposed to falling back on the mainstream position, which is implicitly based on the misleading premises that better international market access, aid and participation in existing multilateral processes will prompt spontaneous economic catch-up and sustainable development. Exposure to undistorted international prices will not alone drive the reorganisation of production or a move towards greater domestic efficiency. Duty-free, quota-free market access has benefited a select few countries. Official development assistance to LDCs is declining and may fall short of objectives.

As structuralists, developmentalists and others have long emphasised, governments and the international community need to promote active measures aimed at building productive capacity. In a power-based global system, developed countries and regions often shape the system of support for LDCs in their own interests – a recognition that is all the more important when commitment to multilateralism is faltering. Dependency theorists stress the importance of power relations and the interdependent nature of the global economic core and periphery. Rather than individual ad hoc assistance or promises of more aid, there is a need for deep-rooted, systemic improvement to the multilateral architecture relating to LDCs – driven by LDC governments themselves and differentiated according to context.

Acknowledging these ideas, this Working Paper proposes six areas of support, relating to the UN system, finance, trade, commodities, technology, and the environment and climate change. Each is accompanied by specific proposals that could be considered in the run-up to UNLDC-V and beyond.

Download (pdf).

By Dan Gay

- The first part of this series showed how rising inequalities in many least developed countries means that for many people graduation is not the end of the story.

- International donors and trading partners could help by further extending international support beyond graduation.

- New post-graduation support measures are also necessary. These measures should prioritise the development of productive capacity; building public finances; tackling environmental vulnerability; south-south technical assistance; and direct cash transfers for marginalised people.

Despite the large number of least developed country (LDC) graduations and the impressive social and economic feats of several graduating countries, inequality is rising. Governments and the international community can still play a part in easing the transition.

This implies stretching international support measures beyond the graduation date. It also means designing new mechanisms for graduating and graduated LDCs.

More of the same

Official donors should be urged to meet their aid targets for LDCs beyond the date of graduation (although paradoxically they already give more development assistance to graduating LDCs than to others, perhaps because they want to invest in faster growing countries where projects earn better returns).

Trade helps ease poverty, and its benefits should not be cut off too quickly, something which is recognised by the Enhanced Integrated Framework, which offers support to LDCs for five years following graduation.

The European Union already extends Everything But Arms (EBA) for a standard three years after a country leaves LDC status – why not longer? European clothing importers order a growing majority of their clothing from the graduating east Asian LDCs, so this should not be too hard a sell. Help could be offered with other preference schemes, such as with putting in place the international conventions necessary to qualify for the Generalised System of Preferences Plus scheme. The United States, too, could expand product coverage of its own preference scheme.

Rules of origin that qualify goods as coming from LDCs are often too stringent, and developed countries might consider extending the simplified terms for LDCs after graduation.

Prolonging flexibilities at the World Trade Organisation (WTO) would also help, such as the exception to the Trade-Related Aspects of Intellectual Property Rights agreement which allows Bangladeshi pharmaceutical manufacturers to copy patented drugs and to issue compulsory licences, exporting cheaply to other LDCs.

The international community could assist former LDCs in joining forces in negotiations. Membership of the LDC group at the UN and WTO, and in climate talks, carries considerable collective bargaining power. The provision of resources contingent on cross-collaboration among trade and climate negotiators would help break down the barriers that often exist between the two groups.

Time for something different

As well as continuing existing support for LDCs after graduation, new, targeted mechanisms for graduating and graduated LDCs should be considered.

Productive capacity remains the main challenge. However much market access they enjoy, most LDCs will always struggle to produce enough – which is why so many run trade deficits.

The international community needs to continue supporting LDCs in accumulating capital, building the technology and enhancing the domestic linkages and entrepreneurship necessary to raise production. Graduating countries can afford to invest more of their total income in building production than many LDCs below the threshold, which must prioritise consumption. Graduating nations also offer particularly receptive territory for technical assistance. Why not a dedicated production transformation fund for all LDCs, with targeted assistance for graduating countries, learning from middle-income success stories?

Public spending remains the best way of tackling inequality, and LDCs often struggle to collect enough tax. In Bangladesh, tax revenues are only 8.8% of gross domestic product, lower than the LDC average. The shortage of state funding for infrastructure is partly why the country’s roads and ports slow development. Public finance management is already a key part of international development assistance. Broadening the tax base helps countries self-finance development and reduces reliance on aid.

Might a dedicated facility for graduating LDCs make sense, particularly at a time when these countries face the prospect of lower aid flows over the longer term? Multilateral efforts to stem tax revenue leakages, to ensure banking transparency and to reform tax havens are at least as important.

In public finance management and other areas graduating countries need good, appropriate guidance from similar contexts. Technical capacity has evolved enough in most graduating countries that policymakers can put nuanced advice into practice. The challenges facing countries on the brink of leaving the LDC category are growing in technicality and specificity. A sufficient critical mass of countries now exists for mutual help on analysis and policy.

Funding for south-south and current and former LDC think tanks should be bumped up in order to build ownership over policy proposals and to tailor any recommendations to the national context.

Prominent institutions in graduating LDCs include Bangladesh’s Centre for Policy Dialogue, the Myanmar Development Institute, Lao PDR’s National Institute of Economic Research and South Asia Watch on Trade, Economics and the Environment in Nepal. Advice should be targeted at different clusters, such as the Asian, island or landlocked nations.

Many of the smaller graduating and former LDCs (like others) struggle to deal with the red tape required for environmental financing. According to the 2016 UNCTAD LDC Report: “While numerous funds have been established for adaptation, this has given rise to a complex architecture of multiple bilateral and multilateral agencies; some of the funds which exist remain seriously underfunded, and accessing funds is complex and time-consuming, particularly for countries such as LDCs with limited institutional capacity.”

While it is important to make sure that money is well spent, institutions like the Global Environment Facility should be urged to simplify their procedures or help recipients with applications. Most graduating LDCs fail to meet the economic vulnerability criterion. Better access to disaster risk insurance, too, would help ameliorate some of the impact on the worst-off.

Reaching the have-nots

Whilst technical assistance is part of the equation, aggregate economic progress does not always reach every section of society. The widening of inequality in so many countries worldwide has prompted many to rethink social inclusion. Handing cash straight to marginalised people may be one answer. A dedicated cash transfer mechanism for graduating and graduated countries could be a critical part of helping ensure that all parts of society are included in economic advancement.

In the larger graduating countries that appear likely to receive less support in the long run, economic growth can exist alongside deepening inequity. In others, like Kiribati, São Tomé and Príncipe, Solomon Islands, Tuvalu and Vanuatu, absorptive capacity for aid is already reaching its limits. These smaller nations, which are often very unequal, have high levels of official development assistance per capita but their governments are often overwhelmed by conventional development funding.

Unconditional direct transfers are a proven solution. Around 130 low- and middle-income countries implement at least one non-contributory unconditional cash transfer programme, either government or donor funded, or both.

Research on cash transfer schemes by donors like the United Kingdom shows that existing cash transfer schemes cut monetary poverty, raise school attendance, stimulate health service use and improve dietary diversity, reducing child labour and increasing women’s decision-making power. Transfers also target the marginalised and lead to more equitable and just outcomes, forming a valuable social safety net for the vulnerable.

Creativity and ambition

Doubtless there are many other ways in which donors and multilaterals could improve help for graduating LDCs, particularly measures that address inequality.

One of the obvious objections is: why not the other LDCs too? And why not middle-income countries facing similar challenges? But official development assistance is already being re-designed anyway under the Financing for Development agenda. OECD DAC donors are seeking to redefine aid to include private flows and blended finance. Now is a prime opportunity to aim new forms of assistance better at the exact demands of graduating LDCs, allowing the needs of other recipients to be addressed more precisely. The stubbornness of lingering inequality in otherwise dynamic nations calls for a more nuanced, targeted approach.

The 2030 Sustainable Development Agenda is clear that new forms of development assistance need to be tailored to the needs of the least advantaged. The private sector, donors and recipients all have an interest in leaving no-one behind.

A touch of ambition, invention and creativity would go a long way. Every person in those dozen graduating countries deserves to share in success.

——-

This article is the second of a two-part series. Part one looks at rising inequalities in Bangladesh and other least developed countries.

By Dan Gay

- Following rapid progress, up to 12 LDCs may leave the category in coming years.

- The countries involved include up to a quarter of the total LDC population. Progress has been underpinned in some areas by international support measures for LDCs.

- Yet lingering – and in some cases worsening – inequalities mean that many people are being left behind.

On the journey south from Chittagong to Cox’s Bazar in southern Bangladesh the dynamism is palpable. A plush new road disrupts the ruts south of the city, funnelling travellers through green rice fields. The traffic is less apocalyptic than in the capital Dhaka but the shiny symbols of a youthful middle class still file past. The battlements of new concrete kingdoms flank the roadside.

On the journey south from Chittagong to Cox’s Bazar in southern Bangladesh the dynamism is palpable. A plush new road disrupts the ruts south of the city, funnelling travellers through green rice fields. The traffic is less apocalyptic than in the capital Dhaka but the shiny symbols of a youthful middle class still file past. The battlements of new concrete kingdoms flank the roadside.

The voyage reflects Bangladesh’s own. Civil war and famine in the early 1970s gave way to a green revolution. Ingenious industrial policies helped build employment in a booming garment industry, and the services sector is now expanding fast. Extreme poverty fell from four-fifths to less than a tenth. The economy will be one of the world’s three fastest-growing in 2019.

Health and education flourished. At independence in 1971 the average Bangladeshi lived to the age of 47. Now, she or he can expect to reach 72, higher than the South Asian average. Infant mortality plunged from 149 to 28 over the same period, also outperforming the region. Nearly three-quarters of children go to secondary school, up from only a fifth in 1973.

These feats of social headway are partly testament to Bangladesh’s legendary civil society. Over decades, non-government organisation workers honed their skills in rural areas. Alongside the UN and government in 2015 this enabled them to house, immunise and feed nearly three-quarters of a million Rohingya refugees at short notice after they walked across the border toward Cox’s Bazar from neighbouring Rakhine state in Myanmar.

A wave of graduation

It is this kind of economic and human advancement that places Bangladesh, by far the most populous LDC, near the vanguard of 12 countries scheduled to graduate from the UN least developed country (LDC) category in coming years.

Bangladesh and Myanmar were the only two to meet all three of the criteria for graduation out of LDC status for the first time at the most recent review of the UN Committee for Development Policy (CDP) in 2018. If these countries continue to hit the targets in 2021 they may graduate in 2024. Five countries are already scheduled to leave the category between now and 2024. Seven more are likely to follow soon after.

If so, after a transition period these countries – and their 270 million people, a quarter of the LDC total – will lose the benefits associated with LDC membership, including preferential trading arrangements; a commitment by rich countries to prioritise LDCs in aid allocations; concessional climate financing; assistance with attendance at international meetings; and UN budget concessions.

The growth of the garment industry in the likes of Bangladesh and Myanmar has been underpinned by duty-free, quota-free market access under the European Union’s Everything But Arms (EBA) scheme since its launch in 2001. Freed from paying tariffs on anything it sends to the EU, Bangladesh has become the world’s second-largest exporter of clothing. Myanmar’s industry has grown tenfold since the country was granted access to EBA in 2013. Over half a million workers send three-quarters of their pay to relatives in the countryside. For Cambodia, too, which is likely to graduate at a later date, EBA has been a boon to garment manufacturers.

Some other LDC exporters also make use of trade preferences. And for those countries that do not, governments are often reluctant to signal complacency by giving up the remaining small symbolic concessions.

Whilst some might say it is time for graduating LDCs to surrender these privileges, the real picture is more nuanced. The playing field is not level. Some former LDCs will still face massive disadvantages of geography, history, size, economic structure and position. A nation may graduate but many of its people will not.

The tyranny of averages

Gross national income per capita in Bangladesh hit US$1,274 on a purchasing-power basis in 2018, just above the threshold for graduation.[1] But dividing total income by the country’s 163 million population does not say anything about distribution.

While poverty has ebbed over the long term, and most Bangladeshis live vastly more educated, healthy lives than after independence, progress is stalling.

The incomes of the bottom tenth of Bangladeshi households fell between 2010 and 2016. The lowest five percent found their incomes falling by more than half over the same period, according to government figures. About 40 million people still live below the national poverty line – enough to make up the fifth-largest least developed country in their own right. Meanwhile the income of the top five percent of urban households rocketed 88%, in 2016 taking home over 100 times more than the poorest.

“The unambiguous conclusion that can be inferred is that the rich are getting richer while the poor are getting poorer,” says a report by the Dhaka-based Centre for Policy Dialogue. As in so many countries, increasing numbers of people are being left behind.

The explosion in the incomes of Bangladesh’s rich allows them to accumulate ever more. The distribution of wealth is stark. A paper by the Centre for Policy Dialogue calculated that by 2010 the top five percent of households owned over half of all the country’s wealth and the top one percent nearly a third. The bottom one percent, in contrast, did not have any wealth and the bottom five percent only 0.04%. The same paper found the wealth Gini coefficient was 0.74, representing severe wealth inequality.

A least-developed state

Across the world the share of wages in economic output is declining, while the returns to capital rise. Globalisation is narrowing differences between countries but opening up chasms within them. The same picture plays out across several graduating LDCs, where an affluent, educated urban class take advantage of the opportunities of industrialisation and international openness, leaving others behind.

Bangladesh is hardly unique. In Vientiane, the capital of Lao PDR, you can order a fine duck breast with foie gras followed by crème brûlée or while away lunchtime over a flat white. Meanwhile in a village of Lantan people in the northern province of Luang Namtha, pot-bellied trouserless children sell wrist-bands to tourists for 80 US cents. Coughing can be heard from inside thatched huts.

Here and in other rural areas, access to the modern economy and social services is worse than in the capital. Indigenous people are often among the most vulnerable. Faced with fewer job opportunities and no other source of income, many more people will in effect continue to live in a least-developed state for many years to come. How should the international community respond?

_____

First published on Trade for Development News.

This column is the first of a two-part series. Part two considers some possible new ways to support graduating LDCs.

[1] The per capita income threshold at the last triennial review was US$1,230 using the World Bank Atlas method on a purchasing power basis. The other two criteria are a human assets index and an economic vulnerability index. A country must exceed more than two of the three criteria at two consecutive reviews of the CDP to be considered for graduation.

Digits won’t replace states

I’m all for new technologies that subvert convention — but i’m cautiously sceptical about this piece on new multilateralism from Anne-Marie Slaughter in the Financial Times.

I love the sentence “while antediluvian men strut back and forth on the world stage beating their chests, a different kind of multilateralism may be on the horizon.”

Slaughter argues that the Internet makes new forms of digital cooperation both imperative and inevitable. A new UN “Declaration of Digital Inter-dependence” signed by business people and philanthropists like Melinda Gates and Jack Ma asks politicians to try to solve specific problems alongside leaders from business, civil society, labour, academia, faith groups, women and other marginalised communities.

It’s a good idea. Digital tools — like, presumably, social media and other forms of instantaneous mass communication — make global new forms of cooperation among these people possible. We should probably also get wise to their potential, because they also raise risks and challenges. “Isis can recruit a global army online, before and after its physical ‘caliphate’ has been destroyed. Companies can create currencies without a national mint or central bank.”

The digital Declaration proposes “new governance structures for the digital world of the future, which will supplement and could ultimately swallow the UN, at least as we have known it.”

Slaughter is quite right that politicians should listen to a range of different groups, and that in the future they’ll probably have no choice but to do so. Conventional democracy confined to nation states is woefully inadequate. We should be voting across international boundaries on issues of collective importance — especially climate change — using supra-national and local structures. Marginalised peoples for the first time have a voice. Technologies exist to allow us to make our voices heard on issues that concern us, from the local to the global. Those issues should be dealt with at the appropriate level rather than abandoned to stale, compromised representatives in a distant legislature which nobody really trusts any more.

We should probably be voting with our smartphones, often, on specific issues that concern us: refuse collection, schools, health, energy, equality. Part of the reason for Brexit and Trump is a power deficit: the old governance institutions of the twentieth century don’t reflect our demands (if they ever truly did). People want a bigger say in how their lives are run, and they’re finding new ways to connect, beyond old physical communities. There’s little doubt that digital space should play a bigger role in multilateralism.

But it’s the forces of power that make me sceptical. As Slaughter implicitly acknowledges, it’s all very well asking politicians to work with other ‘stakeholders’, but politicians do what serves their and their paymasters’ interests. Most probably aren’t going to surrender power voluntarily to other leaders. Social progress is taken, not given.

It’s noteworthy that the Declaration was launched by billionaire business leaders, not ordinary people or grassroots non-governmental organisations. The global 1% spent the last few decades building the plutocracy. Why would they hand over control? In fact, this sort of initiative is probably the billionaires’ way of maintaining it; hegemony in practice.

Despite the potential for liberation in digital technologies, they are controlled and controllable — and the potential source of mass unfreedom. Edward Snowden’s new book speaks with terror about China’s “utterly mind boggling” surveillance capabilities being replicated on the global stage. Closed-circuit television cameras on every street corner feed back to a central, government-run observation centre which also tracks and watches you through your smartphone.

Facebook shelved Libra because of the widespread outcry over its potential harm, and because US Congressmen for once did their job, subjecting it to scrutiny. Because of obvious vested interests and power, the US dollar will continue to hold sway, not Bitcoin.

A more serious problem with the FT piece is that it’s a bit blind to the full meaning of multilateralism — that it’s about several sides sitting down and physically negotiating rules, often about boring, bricks-and-mortar things. Rules, thrashed out between states, often protect the very marginalised stakeholders that Slaughter lists. Here, we argue that multilateralism is a matter of survival for the least developed countries, and that it must cater to their national interests in somewhat technical areas like rules of origin in international trade and intellectual property. The harmful impact of rich countries’ behaviour in macroeconomic management, tax havens, subsidies, climate and immigration must be addressed in global interactions between rich and poor nations: states, not only communities or digits.

The excellent A New Multilateralism for Shared Prosperity published by UNCTAD and Boston University’s Global Development Policy Centre argues that a global green new deal should feature the rather offline tasks of securing full and decent employment at a livable wage; a just society and caring communities; and a sustainable future. None of this implies swallowing the UN, more revitalising it.

That’s not to say that digital space won’t play a role in new forms of multilateralism, or that new communities shouldn’t be brought into discussions. But multilateralism will for some time probably continue to involve real people sitting down in physical rooms discussing often rather mundane, analogue technicalities. I hope that a new form of multilateralism is on the horizon, but in the meantime, unfortunately, the antediluvian white men will continue to strut.

New op-ed on the UN Sustainable Development Goals site.

By Daniel Gay and Kevin Gallagher

The international system governing the environment and economy is under pressure. Globalisation itself is wobbling, to the chagrin of governments in rich and emerging economies. What’s less talked about is the effect on the world’s 47 least developed countries (LDCs), home to a billion people, a quarter of whom live in extreme poverty.

The financial system has long been rusty. Criticism was again this year leveled at the selection process for the heads of the World Bank and International Monetary Fund. Developing-country voices called for an open and transparent process based on a pool of candidates drawn from all countries, rather than only from the United States and Europe. Leadership by the world’s marginalised nations would give them voice, reorientating the Bank and Fund toward their own needs.

Donors aren’t as generous as they used to be — with worse to come after it recently emerged the United States might chop $4 billion from its aid budget. Development aid to LDCs has stagnated in recent years as some rich countries reallocate or cut aid. The latest figures show that support from official donors to all countries fell to US$146.6 billion in 2017 as donors spent less on in-country refugee costs. Only five out of 30 countries from the Organisation for Economic Cooperation and Development (OECD) Development Assistance Committee currently meet their pledges on aid, down from a peak of six.

Recent moves to redefine and repackage development assistance as a joint public-private endeavour have been criticized in some quarters as attempts by official government donors to escape their obligations. The private money mobilised in LDCs is only a third of the global average. Only eight per cent of blended finance goes to LDCs, with most going to middle-income countries. Of the $52 billion directly mobilized by multilateral development banks in long-term private co-financing during 2017, only $2 billion went to LDCs and other low-income countries.

Rich countries aren’t doing as much about environmental breakdown as they should. Support for the Paris Climate Change Agreement has been thrown into doubt despite progress on the work programme over the last couple of years. Any failure to meet targets will have the biggest impact on developing countries and LDCs. Promised adaptation and mitigation funding have often not materialised. LDCs at risk of extreme weather or with a large number of people living in low-lying islands or coastal zones — like Bangladesh and the Pacific islands — are under particular threat. Those countries can’t afford to protect their people from climate breakdown like the rich world can.

LDCs are increasingly unequal, as the urban nouveau riche leave their rural and factory-working compatriots behind. Gender, social and income inequalities remain stubbornly entrenched. Without global coordination, countries have been forced into a race to the bottom on wages, with the poorest countries obliged to slash pay to subsistence levels — or below. Cuts to multilateral agencies such as the UN Population Fund (UNFPA) affected women disproportionately, particularly in developing countries.

But it is in trade where the LDCs may lose most from the new cracks in the international order. The US-China trade war compounds stress on the multilateral trading system, which was already struggling because of a lack of progress on talks at the World Trade Organisation. Bilateral trade and investment agreements have multiplied in recent years, particularly those involving developing countries. Without multilateralism, flawed as it is, LDCs are compelled to accept terms offered by their developed and more powerful developing-country counterparts rather than strike deals collectively as part of a bloc using accepted rules.

Rich countries are negotiating mega-regionals like the Transatlantic Trade and Investment Partnership or the Trans-Pacific Partnership, eroding the value of existing schemes for LDCs and forcing on to the agenda ‘WTO Plus’ issues like strong intellectual property protection, which is contrary to the interests of LDCs.

Some LDCs are doing well. Up to 12 may officially ‘graduate‘ from the category in the next decade, including Bangladesh, Angola and Myanmar, which together account for half of all LDC exports. But many are being left behind. In a decade it is possible that on current trends, the LDC group will consist of about 30 countries in sub-Saharan Africa, plus Haiti, Yemen and Afghanistan.

This ‘Africanisation’ of the LDC group will mean that existing multilateral concessions such as the duty-free, quota-free access provided to LDCs by the European Union under its Everything But Arms (EBA) initiative will soon fade in importance, given that it is largely Asian countries that use the scheme. The EBA initiative, launched in 2001, was a major breakthrough in the relationship between the LDCs and the world’s biggest trading bloc. The abolition of import taxes and quantitative restrictions was worth billions to the exporting LDCs, particularly Bangladesh (the scheme clearly benefited European clothing importers too).

In a decade’s time, unless trade patterns change, the remaining LDC group will export far less to Europe under EBA — and even to developed countries in general under other trade preference schemes. Only a third of LDC exports come from Africa, mostly unprocessed commodities like oil, gas and minerals, some of which are duty-free for all countries. Trade preferences are already hugely under-used, especially by African agricultural exporters. Nearly half of fruit, vegetables and plants could be exported from developing countries under preference schemes but aren’t. Around $4 billion of clothing and mineral trade preferences go unutilised.

LDCs are trading more with each other and with neighbouring countries. The African Continental Free Trade Area signed last year will boost intra-African trade. The rise of south-south commerce is already heralding the end of the era in which trade preferences were dispensed by the developed world to passive recipients. The multilateral regime will have to rebalance even further so that the global South plays a more active role. It’s worth remembering, though, that South-South trade is no panacea. Sub-Saharan Africa’s economy is about the same size as that of France.

If those at the head of the multilateral order want to avoid a damaging schism in which the rich world leaves the have-nots further behind, they’ll have to get inventive. New schemes should be tailored to the needs of individual countries or regions — particularly including measures which make it easier for LDCs to meet the rules of origin required to qualify for preferences. Existing trade agreements need to be made more inclusive, and more sensitive to the needs of LDCs. Trade is about more than market access. Developed nations could best help the world’s periphery by reforming their own practices on climate, tax havens, immigration, subsidies and economic management.

The shift in trade preferences amounts to yet another wrinkle in the multilateral order, one which stems from current trends rather than active challenges to the international system. It comes at a difficult time for the least developed, whose fragile economies are teetering amid global uncertainty. A small downturn in an LDC can be devastating, whereas the worst-off in richer countries have savings and social safety nets — increasingly leaky though they are. Because people in the poorest countries have less room to cushion the impact, they have the most to lose. For people in LDCs, revitalising multilateralism is a matter of survival.

Dr Daniel Gay is an adviser working with the UN Committee for Development Policy on the least developed countries. Twitter: @DanGay

Dr Kevin P. Gallagher, a member of the UN Committee for Development Policy, is director of Boston University’s Global Development Policy Center. Twitter: @KevinPGallagher