Rethinking support measures for the least developed countries

Dried cocoa beans ready for export

International support measures for least developed countries were partly based on the premise that LDCs are artificially or temporarily excluded from the global marketplace due to their recent colonial history, isolation, smallness, vulnerability or due to trade barriers.

In providing assistance measures to LDCs, the international community has tended to focus on global market integration, under the belief that development will accelerate under conditions of full assimilation into the global economy. Many of the development challenges faced by LDCs are believed to be a result of their insufficient exposure to correct market prices and conditions. When so-called market distortions in the form of tariff and non-tariff barriers to trade are removed, and after a temporarily higher period of development assistance, these countries’ economies will, the assumption goes, be freed up to play a fuller role in the international order. The resultant upturn in economic growth will reduce poverty.

This perspective, informed by the same mainstream neoclassical economic theory that is believed to apply in developed countries, partly underlies the design of current international support for LDCs (along with pragmatism, as in what developed countries felt able to offer). To this end, the main international support measure is duty-free, quota-free market access to developed and developing countries. Special trade measures for LDCs date to 1979, with the Enabling Clause which permitted trading preferences targeted at developing and least developed countries which would otherwise violate Article I of the General Agreement on Tariffs and Trade, on most-favoured nation treatment.

The main source of duty-free, quota-free market access for LDCs is the Everything But Arms initiative of the European Union, which grants full duty free and quota free access to the European Union Single Market for all products except arms and armaments. It entered into force in 2001. LDCs also benefit from trade schemes in destinations including Australia, China, New Zealand, the United States and other developed and developing countries.

These measures are seen as the removal of a trade distortion which will bring about greater efficiency. A simple neoclassical trade model, drawn from microeconomics, sees taxes as market distortions, and their removal as bringing about an increase in consumer and producer surplus. In addition to outward market access, considerable emphasis has also been placed on domestic tariff reduction. Mainstream theory in fact goes as far as assuming that wages will equalize between countries over time and as barriers to commerce fall.

Companies in LDCs are in theory supposed to respond to the removal of so-called trade distortions by diversifying, increasing production and/or improving efficiencies (a relative, although declining, margin of tariff preference also gives them an advantage over other countries). The expectation is that exposure to ‘correct’ global market prices would also see the emergence of new enterprises in LDCs aiming to take advantage of better global market conditions.

In addition to duty-free, quota-free market access the second major benefit of LDC membership (in addition to other smaller measures such as scholarships, travel assistance and reduced budgetary contributions to international organisations) is additional official development assistance (ODA) and climate financing. Organisation for Economic Cooperation and Development (OECD) Development Assistance Committee (DAC) members committed to provide 0.15-0.2% gross national income in ODA, higher than the level allocated to developing countries in general. Official bilateral assistance to LDCs totaled $24 billion in 2016, having increased rapidly after 2000 but recently levelling off and declining slightly. Seen as a temporary benefit which will be reduced following graduation from the LDC category, official development assistance and Aid for Trade – explicitly aimed at global economic integration – can be viewed as stop-gap measures aimed at correcting the hopefully short-lived position of LDCs while they undertake full domestic market development or integration into the world economy.

Importantly, under this broad perspective trade is seen not as just one among many facets of development, but as a fundamental – perhaps the fundamental — driver of economic growth, and in turn of development more broadly.

The scorecard so far

The economies of some LDCs are developing quickly. Six new countries met the criteria for graduation for a second time at the 2018 triennial review of the Committee for Development Policy. Of the seven countries to have graduated or been identified for graduation since 1971, six have done so since Cabo Verde in 2007. By 2018, in total 10 countries, or approximately a fifth of the countries on the list, either had left the category or been identified to leave. Bangladesh, Lao PDR and Myanmar were regarded as likely to meet the criteria for graduation for the first time in 2018. At least three others appeared ready to follow soon after.

However 10 graduations in half a century is too few to meet global objectives. The countries that have graduated so far have not all done so as a result of better international market access. The performance of the LDC group as a whole has been mixed. Since 2000, gross national income per capita in LDCs has consistently grown more slowly than in the group of middle income countries (some of which are also LDCs), even if it outstripped world income growth. In almost a third of LDCs GNI per capita declined between the 2015 and 2018 triennial reviews of the Committee for Development Policy (although inflation, exchange rate changes and data revisions affect the numbers). The human assets index scores of 40% of countries fell between the 2015 and 2018 reviews. Almost 45% of LDCs experienced an increase in their economic vulnerability scores. Data issues may exaggerate these proportions, but the picture is far from uniformly positive.

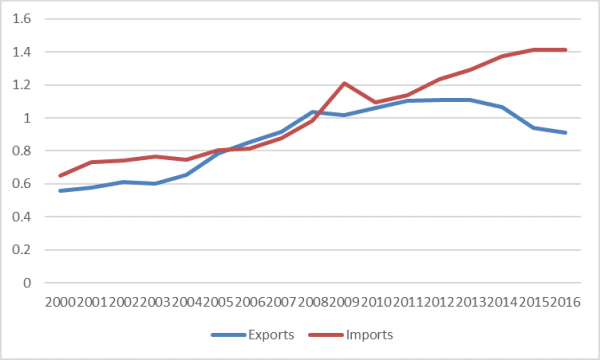

LDCs have not overall benefited as much from trade as expected. Countries like Bangladesh and Cambodia appear to have developed the productive capacity to take full advantage of duty-free, quota-free market access, but many of the less advanced LDCs have not, and most LDCs have been hit particularly hard by the collapse in world trade after 2008. LDC imports have grown considerably faster than exports in the last decade, and LDCs’ collective share of global merchandise exports was no higher in 2016 than a decade earlier, at 0.91%. Trade per capita remains very low: the 47 LDCs comprise 13% of the world’s population.

Least developed countries’ share of global merchandise exports and imports, 2000–2016 (Percentage)

The group as a whole is highly diverse, ranging from the commodity-dependent sub-Saharan African members, to the Asian countries, which feature more manufacturing, to the tourism-orientated small island states of the Pacific. However most LDC economies tend to be undiversified and their exports dominated by a small number of products, many of which are unprocessed. The volatile nature of international commodity prices remains a major source of economic vulnerability. The countries at the global periphery, to which the LDCs belong, remain defined to some extent by their reliance on commodity production and its unprocessed export to core countries. More than 40 per cent of LDCs depend on commodities for over 30 per cent of their exports, and more than 20 per cent rely on commodities for over half of their exports. For landlocked developing countries, commodity dependence is even more stark.

Commodity dependency index, 2016 (Percentage of countries)

Despite many years of increasing exposure to international market prices via duty-free, quota-free market access, and despite the commitments of developed countries to transfer of a greater proportion of aid to LDCs than to other developing countries, structural transformation is not taking place. A small number of countries, largely small island developing states, have undergone global integration in the form of a tourism upturn and associated investment. However even the graduating countries are doing so not on the basis of a shift toward more ‘efficient’ production or greater integration into the global marketplace, but in many cases as a result of a commodity-price upturn.

Indeed the evidence suggests that many LDCs, particularly in Africa, are undergoing reverse transformation, with a premature shift of the labour force into services, often informal. Conventional structural transformation into higher value-adding activities – often driven by a move from agriculture into manufacturing — is not occurring, with a corresponding impact on productivity. Unemployment and semi-employment remain extremely high in some countries.

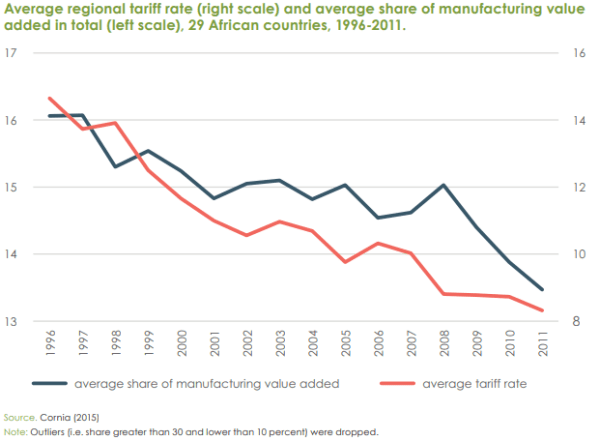

In Africa the decline in manufacturing has even coincided with tariff reduction, as shown by the following diagram, which shows tariffs and manufacturing value-added from 1996 to 2011. Whether or not the relationship is causal, there is little doubt that the decline in manufacturing occurred at the same time as external and national tariff liberalization.

Anecdotal evidence from interviews with manufacturers and other exporters in LDCs reveal that in fact duty-free, quota-free market access, although welcome, is a small incentive. Much bigger issues cited are the lack of investment in infrastructure, exchange rate risk, absence of access to financing and exclusion from global supply chains. Indeed the increased openness to international trade flows, which are volatile, has in many cases been a curse rather than a blessing. This is not to downplay or criticize the role of trade in economic development – indeed trade remains a fundamental driver of poverty reduction and wellbeing – but it does raise questions about the approach so far, and, together with the new era ushered in by Agenda 2030, it may imply the need for a new approach.

Based on this analysis, part II considers alternative ways of thinking about the international support measures for the contemporary era.

Trackbacks